This article was originally published on Forbes on January 5, 2021.

New Changes for IRA and 401(k) Owners Likely Overhyped

It’s been almost two decades since the IRS updated the life expectancy tables that govern IRA distributions. These tables calculate your annual required minimum distribution (RMD), which is the rate at which retirees over a certain age, now 72, must withdraw income from their retirement accounts or face stiff penalties. To reflect a longer-living population, changes will be made in 2022 to lengthen the period of time over which distributions are required, and it will result in lower distributions at each age.

This update comes after the recent SECURE Act, which bumped the starting age for required minimum distributions from age 70.5 to 72 for most retirement accounts.

So, how much of a difference do these changes make to the bottom line?

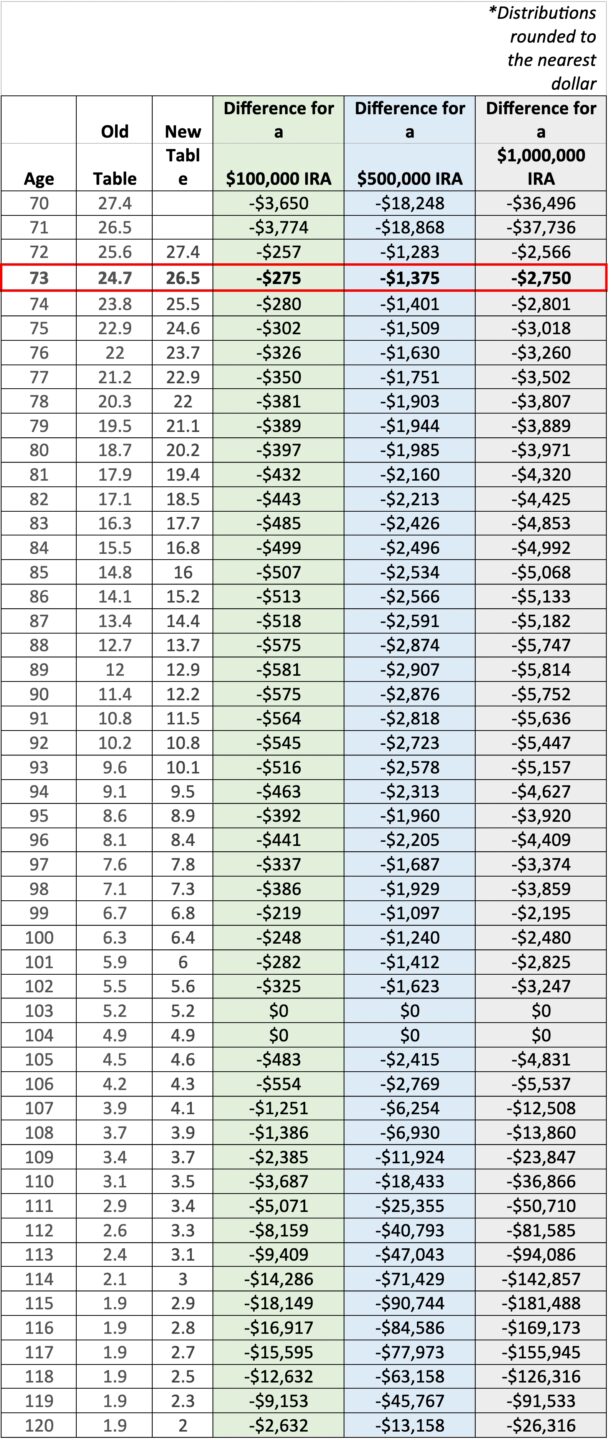

Not much, relatively speaking. To illustrate the difference for an account balance of $100,000, $500,000, and $1MM, check out the table below. Aside from the big change of shifting the starting age from 70.5 to 72, the difference between the old and new calculations is pretty small. Between the ages of 72-100, the difference is barely a half a percent of the account balance.

For example, for a 73-year-old with a $500,000 IRA, under the old calculation they were required to withdraw $20,243 (calculated by dividing $500,000 by the table factor of 24.7). The new calculation, dividing by 26.5, results in a withdrawal of $18,868, or $1,375 less. That means the retiree can take their new, lower distribution and pay less in taxes.

But wait, doesn’t that mean less income for retirees? Not necessarily. If the retiree chooses to withdraw more, they can do so. This is only the minimum amount they must withdraw. The catch is that, with few exceptions, IRA distributions count as ordinary income on your tax return. All else being equal, you’ll usually pay less in taxes if you can pull money from other sources first, such as cash savings or a brokerage account.

Plus, the recent rise in the stock market has boosted many IRA balances. With a higher balance, a higher distribution is required, perhaps offsetting all or more of the drop caused by the new calculation method.

What does that mean for the average retiree with a few hundred thousand dollars saved? Not much. Their IRA custodian will continue to calculate their RMD each year based on the balance at the beginning of the year. Beginning in 2022, that calculation will be slightly different. For most investors over 72, the difference will be small and is likely impacted more by two things: 1) the performance of their investments and 2) their increase in age.

All in all, there’s little reason to worry about the coming changes to your RMD.