This article was originally published on Forbes on December 2, 2020.

The US Government has been spending and printing a lot of money to help stabilize the economy during this tumultuous 2020. As such, several of my clients are once again raising their concerns about inflation. Most of these worried clients fit into a certain demographic who remember the runaway inflation at double-digit levels in the early 80s. Mortgage rates, they recall, and remind me often, were as high as 18% back then. And given the nearly incomprehensible amount of money being pumped into the US economy, their logic is certainly reasonable.

But hear me out – it’s not that inflation isn’t a concern, it’s just that we are far from it. And COVID changes everything.

We will likely see inflation at some point in the future, but until this one indicator changes, we probably need to calm down about prices moving much higher.

The indicator to watch is wage inflation. The more people are paid, the more they are able to spend and bid up prices. In addition, as workers are paid more, companies need to pass on those higher employment costs to consumers in the form of higher prices.

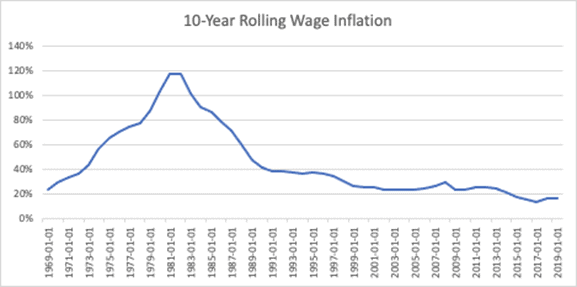

Below, you will see the 10-year rolling wage inflation. Workers saw their pay more than double from 1971-1981. Many argue that wages needed to increase to support higher overall prices. Yet, wages began their ascent in the early 70s, well before measures of high inflation took off.

Source: St. Louis Fed, Glassman Wealth Services

So how does COVID change this dynamic? Suddenly, two huge business expenses have been altered forever. First is the amount, location, and cost of real estate (office space) needed for company operations. As an example, think about the big investment banks in New York City with their enormous buildings essentially empty but still operating nearly uninterrupted as they transact business throughout the world. Put simply, there is less demand for real estate as companies shift their footprint from physical to digital offices – or at least some form of hybrid.

Next is the location of each employee. If Facebook doesn’t need to pay Silicon Valley compensation to entice someone to physically work there and pay sky-high rent, then they will likely cut costs by hiring elsewhere. The sheer number of service businesses that realized they can thrive without a metropolitan office building will impact the largest cost to employers – payroll – forever. An expanded hiring pool across regions, coupled with an excess of people searching for work, leaves ample room for labor markets to tighten before wages can soar.

One caveat: we could see a rotation of inflation from the big cities (NYC / San Francisco) to smaller markets like Austin and Boulder and even countries like Costa Rica. As smaller local economies see increased demand, prices may increase in those markets, but likely not enough to impact overall inflation across the country.

A real risk is that there is a surge in economic activity as vaccines are distributed and widely adopted. We could see enormous pent-up demand for GTFOOTH spending (Get the F* Out of the House). The money for this would not necessarily need to come from higher wages. It could come out of savings, stimulus payments, and cash built up during the pandemic. Yes, even while so many small business and workers have struggled, cash has built up on balance sheets.

Also, keep in mind that while there have not been opportunities to spend, excess cash has also gone into paying down debt.

Ultimately, if we see inflation, it will likely be localized by city and personal to each household. Those looking to renew their rental apartment in Austin will have a very different inflation profile compared to a retired couple with no mortgage. Inflation for the first may be dramatic as more money flows from other major cities, but inflation for the latter may be muted with most inflation coming from wants vs. needs.

Inflation remains a risk on the horizon, but like so many other facets of our lives, COVID has hit the pause button.